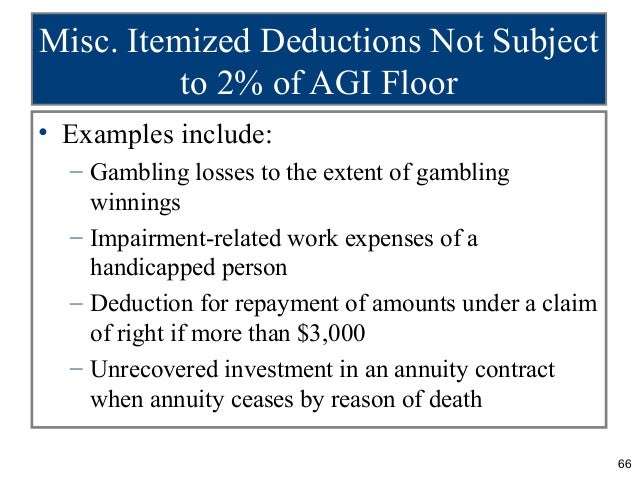

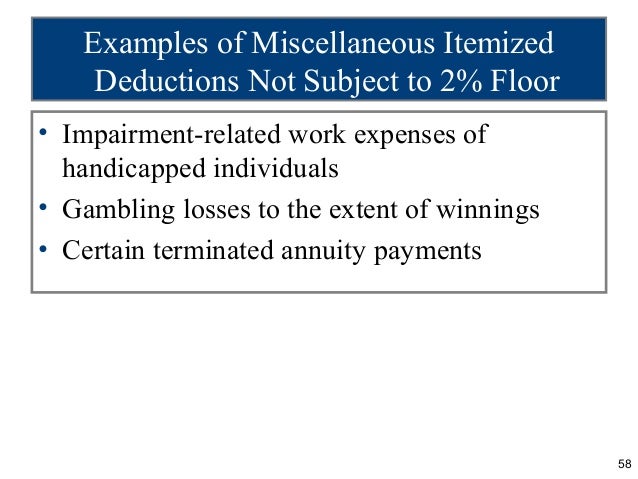

Deductions Not Subject To The 2 Floor

Form W 11 Number 11 11 Common Mistakes Everyone Makes In Form W 11 Number 11 Form W 11 Number 11 11 Common Mistakes Everyone Makes In For How To Get Money Irs

Vol 01 Chapter 10 2015

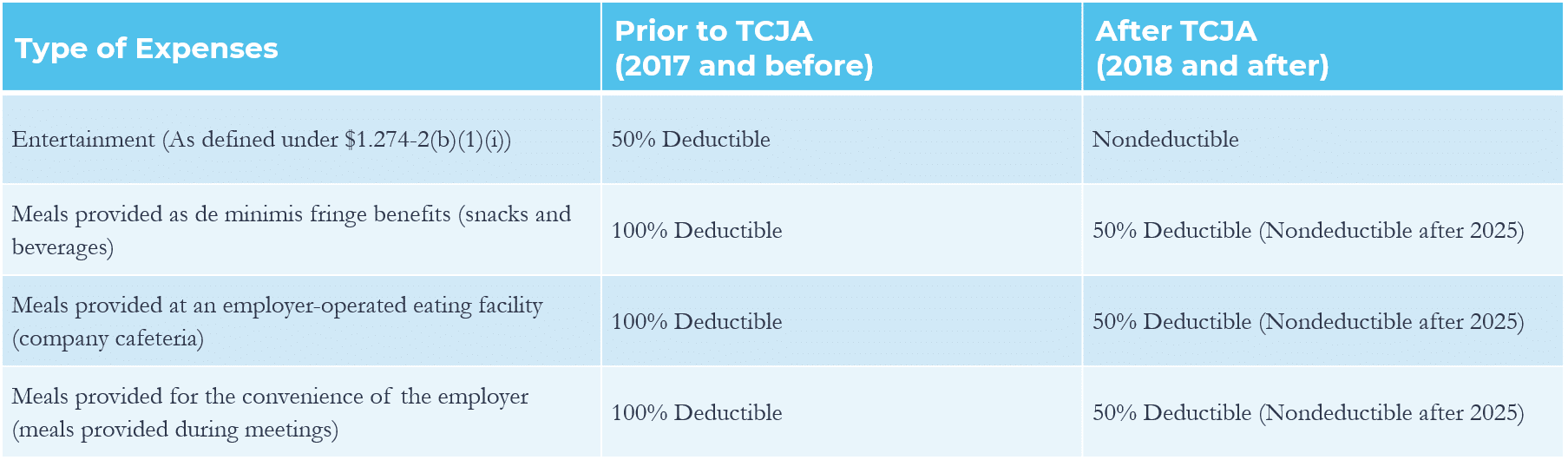

Navigating The New Meals And Entertainment Deductions Under Tcja Grf Cpas Advisors

To Know The Tax Benefits Provided To First Time Home Buyers Watch Out Image Below To Grab These Benefits Just Call Out 8852 Finance Loans Loan Investing

Tax Benefits Are Just One Of The Awesome Advantages Of Having Your Own Home Based Business The Home Based Business Successful Home Business Internet Business

Acct 426 Tax I Chapter 10 Flashcards Quizlet

Investment advice safe deposit box rentals service charges on dividend reinvestment plans and travel expenses.

Deductions not subject to the 2 floor.

Tax Deductions For Individuals A Summary Everycrsreport Com

Potential Tax Benefits With Images Disabled Children Williams Syndrome Parenting

Check Out All The Things Educators Can Deduct From Their Taxes Save Those Hard Earned Dollars Teache Teacher Tax Deductions First Year Teaching Teacher Info

Acct 421 Chapter 9 Flashcards Quizlet

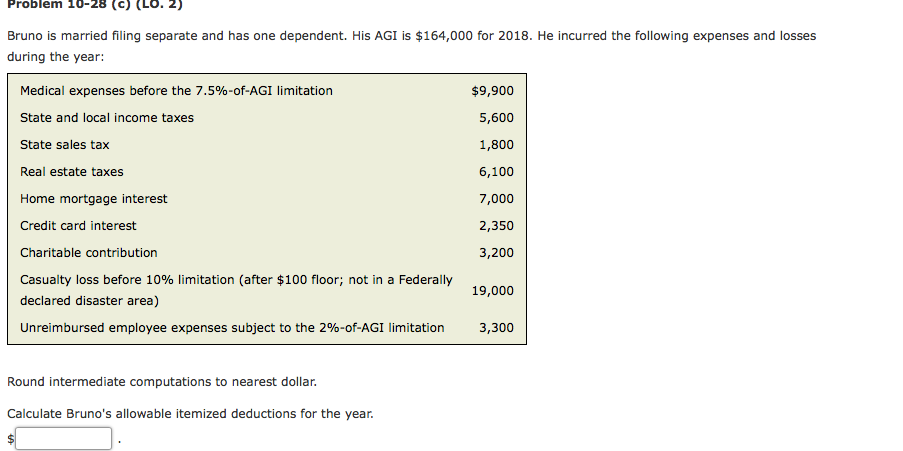

Solved Problem 10 28 C Lo 2 Bruno Is Married Filing Chegg Com

Ppt Ch 09

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Mending The Piggy Bank Budgeting Spreadsheet Budget Spreadsheet Budgeting Spreadsheet

Acct321 Chapter 06

Buffer A Smarter Way To Share On Social Media Backyard Views Garage Style Backyard

709 S Walnut Street Floor Trim Marysville Hardwood Floors

Essay Reflection Goals And Graph By Wondering With Mrs Watto Create Student Accountability And Lifelong Writers The Essay Essay Writing Process Graphing

2013 Cch Basic Principles Ch06

Month To Months Residential Rental Agreement Free Printable Pdf Format Form Rental Agreement Templates Lease Agreement Free Printable Room Rental Agreement

Income Tax Planning And Administration In Decedent S Estates Ppt Download

What Is The Standard Deduction Vs Itemized Deduction H R Block

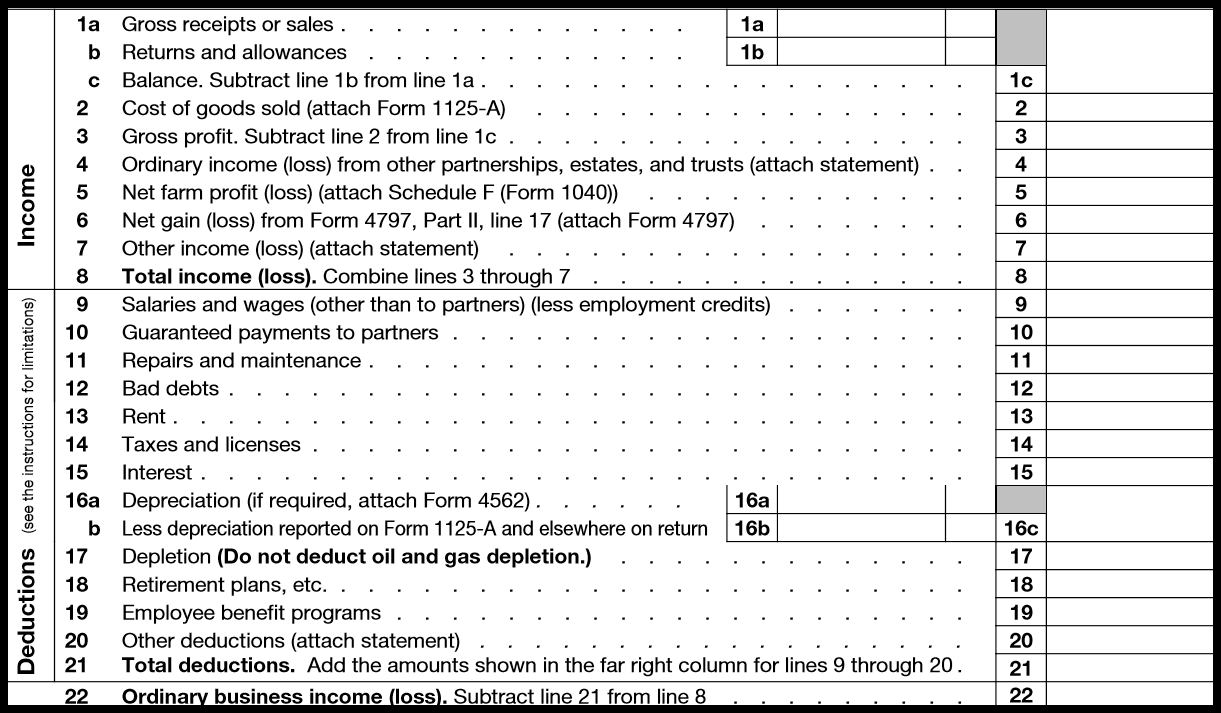

Form 1065 Instructions In 8 Steps Free Checklist

Pin On Airbnb Tips

Proceed With Caution When Making Pay Deductions For Salaried Employees

Notice Of Late Rent Free Printable Documents Late Rent Notice Rental Property Management Rent

Consignment Agreement Google Search Consignment Shops Consignment Business Savvy

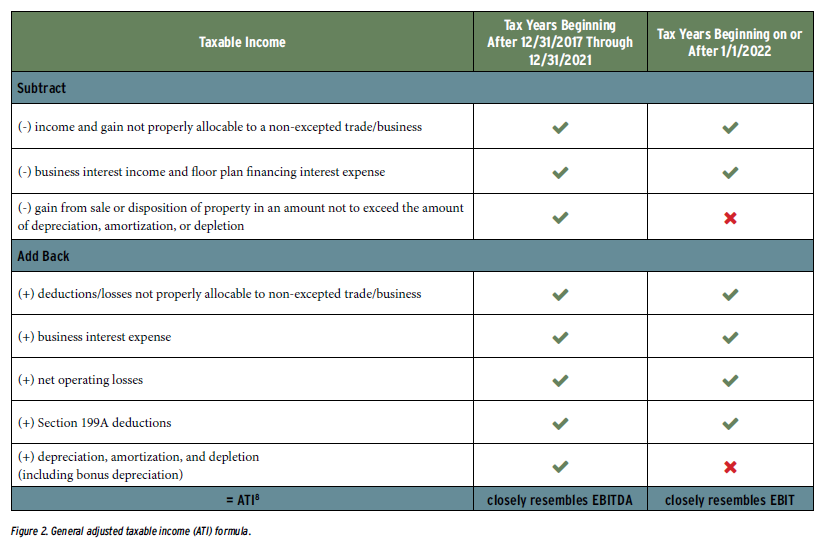

Part I The Graphic Guide To Section 163 J Tax Executive

Printable Sample Free Printable Rental Agreements Form Lease Agreement Rental Agreement Templates Room Rental Agreement

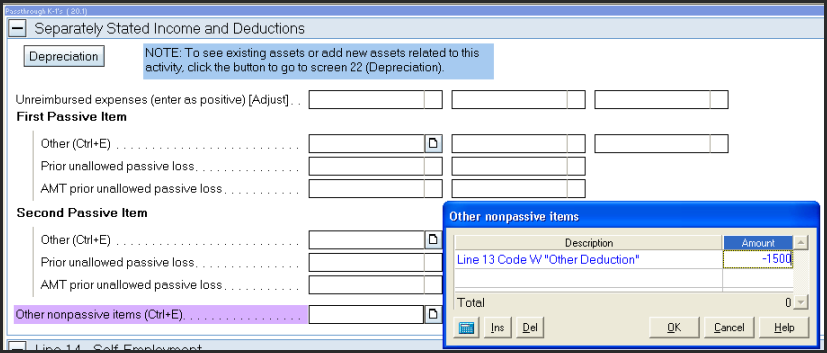

How Do I Report Partnership Schedule K 1 Box 13 Co Intuit Accountants Community

Source : pinterest.com